Pay Yourself First

- Jeff Hulett

- Nov 18, 2023

- 5 min read

Updated: Nov 26, 2023

This is the 3rd article of our budgeting and financial planning series for the month. As a reminder – we grounded the budgeting and financial planning journey in attitudes and behaviors. Next is the “short version” of my approach to wealth building. If you can implement these, you will build wealth.

This is called the M-T-P

Motivation grounding: Be content with yourself, don’t spend money you don’t have, don’t buy things you don’t need, and don’t focus on impressing people.

Time frame setting: Have a long-term focus (and long-term is not two or three years). Wealth and security are built over decades, not months.

Process implementing: Save → Invest → Evaluate → Rebalance → Repeat

About the author: Jeff Hulett is a career banker, data scientist, behavioral economist, and choice architect. Jeff has held banking and consulting leadership roles at Wells Fargo, Citibank, KPMG, and IBM. Today, Jeff is an executive with the Definitive Companies. He teaches personal finance at James Madison University and provides personal finance seminars. Check out his new book -- Making Choices, Making Money: Your Guide to Making Confident Financial Decisions -- at jeffhulett.com.

Please check out Jeff's YouTube channel for the VidCast of this article.

Today we are going to dig into the M or Motivation part of the M-T-P. It is an attitude and approach called “Pay Yourself First.

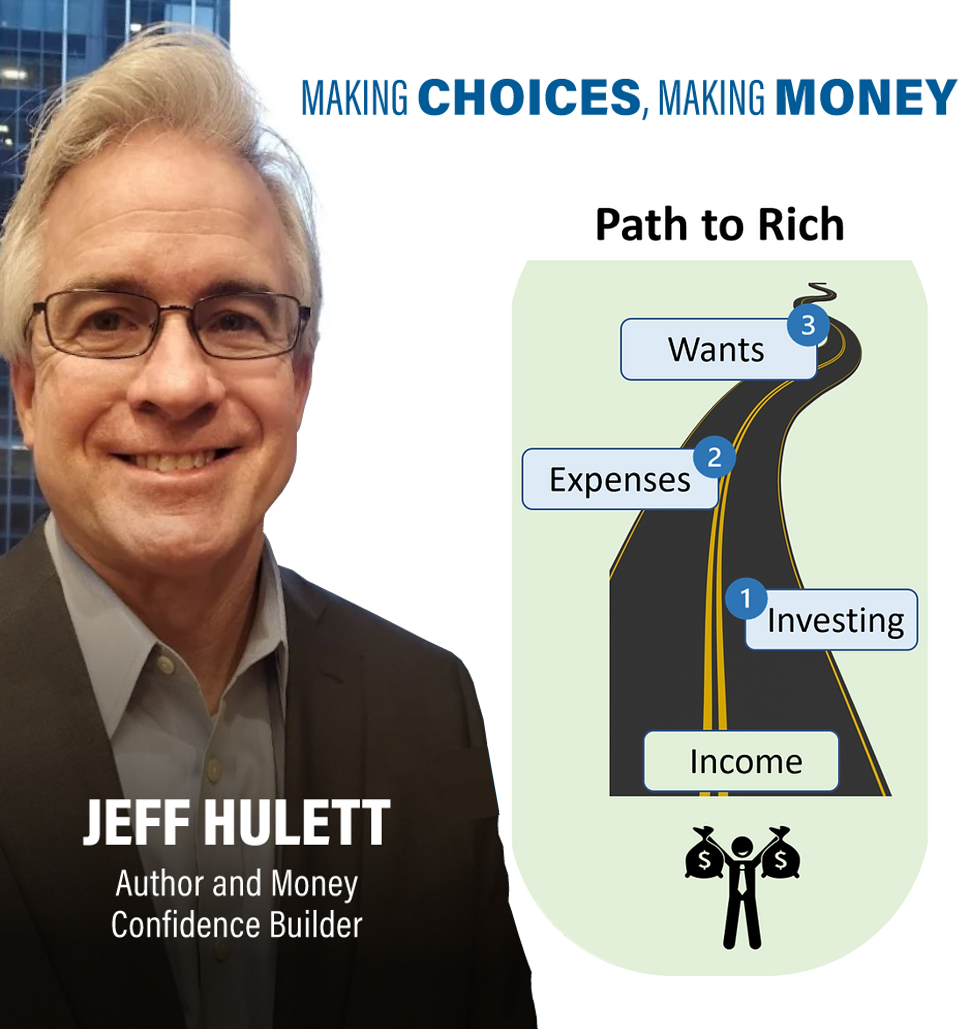

There is a bit of psychology to this aphorism. Here is the thing, typically, your monthly income is fixed. Most of your bills and expenses are fixed. These bills should represent your needs. Next comes your fun money or wants and then your savings and investments. This order is called a "payment hierarchy." If your savings and investments are last, like a leftover, you may never save anything. It is amazing how quickly fun spending can suck all the air out of your investment intention. In fact, most Americans save very little, as this Federal Reserve graphic shows. So, Paying Yourself First helps you achieve long-term wealth and security.

But most Americans do NOT pay themselves first. This means, to better save for retirement, their payment hierarchy needs to be adjusted. Pay yourself first by setting up auto savings and investment transfers from your paycheck. Next, your expenses and bills are the priority, with fun money wants being the leftover. Just changing payment priorities and attitudes can make a HUGE difference in your savings and long-term wealth.

By the way, the little psychology trick is the auto transfer. It is also called a “Commitment Device.” Behavior science teaches us that commitment devices work great! If you never see the money in the first place, the default choice becomes only to spend on wants after proper saving is achieved. This "spend-smart" habit creates an environment where want spending is not even missed.

This is like a forcing function to ensure your savings are at the top of the payment hierarchy. Richard Thaler, the Nobel Prize-awarded Behavioral Economist, made his career on a similar concept for 401(k) retirement savings. It works! Notice the 3 different wealth paths. In this example, there is no difference in income. The only difference is payment hierarchy. The path on the far side is the “Path to Rich.” It is the path where you PAY YOURSELF FIRST!

Now that you are paying yourself first, how much should you pay yourself? I recommend a process called the 'Savings Waterfall" to transition your income to long-term investments. Start with maximizing your company match for the 401(k). Many companies will match up to 5 or 10%. This is free, pre-tax money! Do as much of this as you can! After that, build after-tax savings. Your savings should generally be geared toward an investment fund like a robo-advisor. There are many good robo-advisors. We provide suggestions on the website. Choose a robo-advisor with an auto transfer. I would save and invest 10-20% after tax (or more if you can).

By the way, I'm not a huge fan of the large “6-month” emergency funds that many advisors suggest. I'd rather get a higher investment yield than a low-yielding checking account. You can always use your after-tax investments in a pinch. I’d say, keep no more than 1-2 months of salary to manage your liquidity needs in a checking account. Next, during this transition phase, I recommend a high-yield savings account as a 1-2 month buffer. The last stop on the Savings Waterfall is your long-term investments. With this approach, you will have confidence you are achieving both long-term investment goals AND short-term life liquidity needs.

Also, when you get an annual salary raise, take it off the table. In other words, increase your retirement and after-tax savings by an amount similar to your raise. Why? Your expenses are generally fixed and you have already managed your budget to pay your existing bills. As such, additional "raise" money should be directed to savings and investments. This is a cornerstone activity for "Pay Yourself First!"

You can find this graphic and other information in my book. The "Savings Waterfall" is the framework for transitioning this month's "Pay Yourself First" savings from your checking account to your long-term savings and investing.

Our "Savings Waterfall" helps you implement the P or “Process-implementing” from the wealth-building approach discussed earlier As a reminder:

This is best facilitated by setting up auto transfers between the waterfall buckets. The best part about it is that the robo-advisor does the heavy lifting "Invest → Evaluate → Re-balance → Repeat" part. All you need to do is "Save →" and transfer the money - the robo does all the rest! This is easily done in commonly available financial apps and bank accounts. Robo-advisors have super low minimums and are easy to set up. Start small and build! After starting, you will discover more options. Most robo-advisors also have special accounts for different long-term life "buckets." These are accounts such as 529 College Plans, Roth IRA's, target date investing accounts for specific needs, and others.

So what is the payoff? Earlier we discuss coffee-nomics and the power of the time value of money with a small coffee expense. The Pay Yourself First pathways are significantly more meaningful. This graphic provides the results when we model all three Pay Yourself First pathways. As expected the difference is extraordinary. In this model, each person's lifetime salary is exactly the same! All we did is change the payment hierarchy savings habits. We provide the link to our model in case you wish to play with the assumptions. The point is, your payment hierarchy habits are incredibly important, especially earlier in your career!

Next time, we will be discussing the impact of sludge and tactical approaches to managing your budget.

Notes

All source citations are found in the article:

Comments